November 17, 2022

Public Cloud Horse Race Heating Up: Gartner

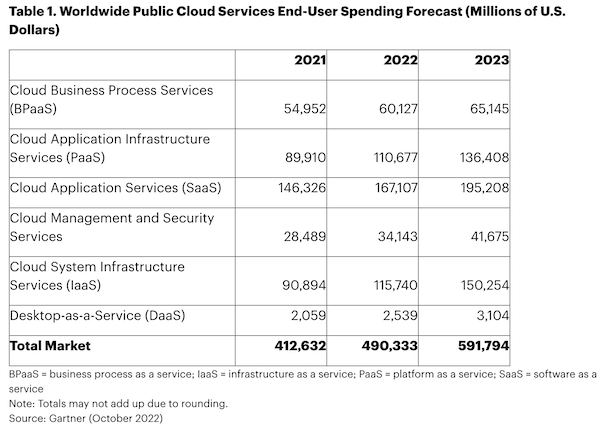

Gartner predicts that worldwide end-user spending on public cloud services will grow to $591.8 billion in 2023, a 20.7% growth from 2022. The public cloud horse race has several cloud services companies jockeying for position, and Gartner’s recently released 2022 Magic Quadrant for Cloud Infrastructure and Platform Services ranks the strengths and weaknesses of the top eight.

The cloud infrastructure and platform services (CIPS) market consists of standardized, highly automated offerings in which infrastructure resources such as compute, networking, and storage are complemented by integrated platform services (managed application, database, and functions as-a-service offerings), according to Gartner.

“The market for CIPS is changing in significant ways that have long-lasting ramifications to the future of enterprise IT. The hyperscale cloud providers are in a race to colonize enterprises in an attempt to become the primary strategic supplier of cloud services to address a broad range of IT workloads,” the report states.

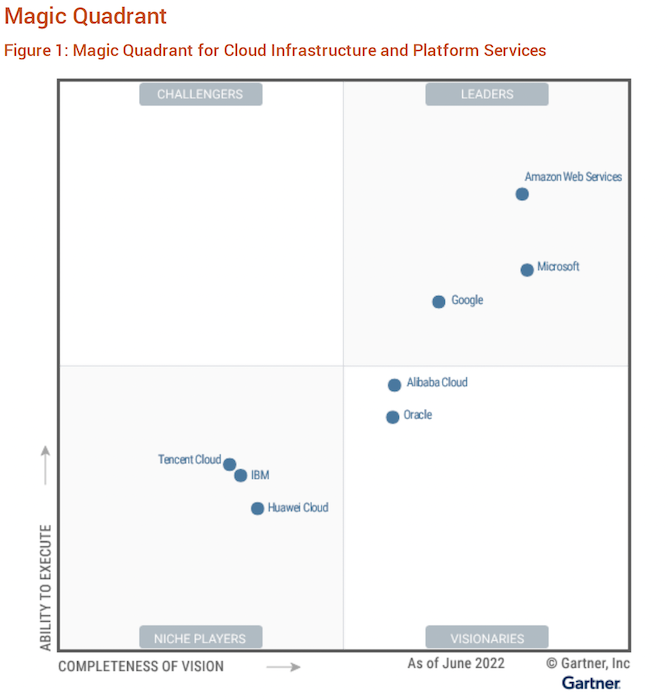

Gartner’s 2022 Magic Quadrant for Cloud Infrastructure and Platform Services. Source: Gartner

Gartner says that the ultimate goal of cloud providers is to move enterprises further up into the PaaS layer where margins are higher and extricating workloads and processes is more difficult. The firm warns that negative consequences of enterprises being locked into a single cloud provider are beginning to surface in the form of higher spending and software licensing woes: “Gartner client inquiry across a broad array of worldwide regions reveals unscrupulous behavior on the part of the cloud provider once enterprises are fully locked-in. Some cloud providers use strong-arm tactics to force enterprises into agreeing to increasingly higher committed spend levels. Others use software licensing from an entrenched base of operating system and relational database management system utilization to direct more cloud usage to their respective offerings,” the report disclosed. Though some enterprises are resisting this through IT supplier diversification, Gartner says, complexity and overhead challenges are often resulting in a multi-cloud strategy that can actually increase TCO.

The report looks at companies’ understanding of the markets they serve, marketing and sales strategies, product strategies and innovation, the soundness of business models, vertical/industry strategies, and geographic strategies through which they can meet specific needs of users outside of their native locations through partners, channels, and subsidiaries. These aspects determine which companies have the most complete vision and abilities to execute it and give a basis for customer consideration.

“I&O leaders must weave through a perilous environment consisting of increasingly aggressive cloud providers further complicated by rising inflation, competition for cloud talent, regulatory mandates, and security and downtime incidents,” the report states.

Read on to see how the players in this fiery market have ranked.

Leaders

Amazon Web Services has the greatest breadth and depth of capabilities in the CIPS market, Gartner says, due to it serving as a guide in the general market by setting standards, developing technology, and establishing methodologies that are repeated by other cloud providers. AWS is the current market-share leader with two times the revenue of its closest competitor, Microsoft Azure. Additionally, Gartner recognizes that AWS does not pad its sales numbers with offerings outside the realm of cloud services such as OS licenses and on-prem PaaS platforms. The company is also recognized for its partner ecosystem which includes SAP, Splunk, and VMware.

The report cautions users that AWS client practices can erode its customer relationships. Client relations are sometimes optimized for the short term, and contract renewal can be tricky, especially with frequent executive management changes and changing customer priorities. Gartner also warns that AWS seems averse to multi-cloud and sovereign cloud strategies, even though many of its customers also use other cloud vendors. Regional dependencies, outages, and poor communication also made the list of Gartner’s concerns.

Microsoft is another leader on the quadrant, with Gartner reporting Azure is strong in all use cases including extended cloud and edge. Microsoft has made heavy investments on hybrid and multi-cloud, making architectural and security improvements on its geographically diverse Azure platform. Its strength lies in its market share as it works to close the gap with AWS, which Gartner predicts will significantly shrink within the near future as evidenced by the European market. Microsoft Azure is also solutions oriented with an extensive range of cloud capabilities and ecosystem partners that facilitates use cases in telecom, healthcare, manufacturing, retail, and financial services, states the report.

Microsoft is another leader on the quadrant, with Gartner reporting Azure is strong in all use cases including extended cloud and edge. Microsoft has made heavy investments on hybrid and multi-cloud, making architectural and security improvements on its geographically diverse Azure platform. Its strength lies in its market share as it works to close the gap with AWS, which Gartner predicts will significantly shrink within the near future as evidenced by the European market. Microsoft Azure is also solutions oriented with an extensive range of cloud capabilities and ecosystem partners that facilitates use cases in telecom, healthcare, manufacturing, retail, and financial services, states the report.

Gartner’s report advises that security issues and lack of innovation are Microsoft Azure’s main weaknesses, as well as opaque costs and lagging cost management and cloud cost optimization capabilities. Gartner also notes that Microsoft is punitively using product licensing against competitors by making it more expensive to deploy Windows workloads elsewhere than Azure while not communicating licensing restrictions to customers, such as restrictive rules under Azure Hybrid Use Benefits in Azure multitenant environments.

Google Cloud also made the leader list. The report says its Google Cloud Platform is strong in nearly all use cases and has made significant improvements in its edge capabilities. The company’s strengths include its revenue and capabilities gains, as its cloud platform saw the highest percentage of revenue gains and improvements across Gartner’s Critical Capability for CIPS. “This is largely the result of increased field sales, co-selling with partners, and a commitment to offering a competitive platform from the perspective of capabilities,” the report states. Google Cloud has also been focusing more on the enterprise with a shift to selling to business executives over technical teams, showing how enterprises are now considering it a legitimate supplier of enterprise IT solutions.

Weaknesses of Google Cloud include its increasing prices, with some aspects of its storage services rising by 100%. “While Google is honoring existing customer commitments, this event is notable for being the first significant increase of published pricing by a provider in this market,” Gartner says. The company has also experienced financial losses, despite revenue gains, as Gartner reports it is the only CIPS provider with a significant market share that continues to currently operate at a large financial loss.

This table from another recent Gartner report shows the revenue at stake in the public cloud horse race. Source: Gartner

Visionaries

Alibaba Cloud is ideal for cloud-first digital business workloads for customers based in China or Southeast Asia, Gartner said of this Visionary. The company’s international business headquartered in Singapore was the focus of this Magic Quadrant evaluation. Strengths include the company’s regional and engineering leadership, its ISV partnerships with SAP, VMware, IBM, and Salesforce, and its digital transformation and commerce capabilities. The company’s success has been impeded by regulatory pressure from Chinese authorities and its competitors, according to Gartner, with its market share being challenged by more government-affiliated cloud providers. There is also a lack of a rich MSP ecosystem, along with limited or unevenly managed partner programs within and outside of China. Gartner also highlights inconsistency and opacity in pricing and capabilities for international customers compared to its Chinese offerings and noted that pricing for the company’s various tiers is often disproportional.

Oracle, a Niche Player in last year’s Magic Quadrant, is now a Visionary. The company has focused its Oracle Cloud Infrastructure on hybrid and multi-cloud, HPC, and cloud migration. “Multi-cloud architectures, where one workload spans multiple cloud providers, are central to OCI’s vision and its future offerings that live within and alongside providers such as AWS and Azure,” the report says. Gartner says the company’s business model innovation in regard to sovereign clouds and other emerging enterprise needs is valuable for enterprises in countries with strict regulatory and data privacy requirements. Gartner predicts that Oracle will meet or exceed some Leaders in terms of hyperscale cloud capabilities in the near future if its current year-over-year pace of feature velocity continues bringing it closer to market leaders.

However, years of inconsistent sales and support have given the company a negative brand image, states Gartner, which has hindered eagerness to use the platform. Other concerns raised by the report include how OCI’s sales and partner networks are not suited for addressing non-Oracle workloads and are not seen as a general-purpose solution for all enterprise workloads.

Niche Players

Niche Players

IBM, Tencent Cloud, and Huawei Cloud are this Magic Quadrant’s Niche players. IBM’s cloud operations are geographically diversified and focused on extended enterprise use cases. The company has a strong vision for modernizing enterprise workloads and its container management through OpenShift is a foundation for delivering jointly branded offerings with other cloud providers, Gartner says. IBM has had reliability hiccups lately, though, as well as issues with competitive identity and a less comprehensive sovereign cloud strategy.

Tencent Cloud combines a portfolio of IaaS services optimized for high-performance networking and scale-out application architecture, combined with pricing and support models that are customized for strategic high-value customers, says Gartner. But questions remain about its long-term commitment to large enterprise customers with general IT workloads, as well as its limited partner ecosystem and modest market share gains due to limited innovation.

Joining the Quadrant for the first time this year is Huawei Cloud, and Gartner highlights its market share strength as the second largest cloud provider in China, its expertise in flexible on-prem and edge deployments, and its enterprise pedigree. International sanctions have tanked its overall revenue by a third, and its immature PaaS offerings and limited partner ecosystem are reasons to be cautious, according to the report.

Access Gartner’s 2022 Magic Quadrant for Cloud Infrastructure and Platform Services at this Google Cloud link.

Related Items:

Cloud Getting Expensive? That’s By Design, But Don’t Blame the Clouds

As Cloud Coverage Expands, Salaries Also Rise

2022 Big Data Predictions from the Cloud

Technologies:

Cloud

Sectors:

Financial Services, Government, Healthcare, Manufacturing, Retail, Science, Telecommunications

Leading Solution Providers

Tabor Network

Sponsored Multimedia

Featured Events

-

AI & Big Data Expo North America 2024

June 5 - June 6Santa Clara CA United States

June 5 - June 6Santa Clara CA United States -

CDAO Canada Public Sector 2024

June 18 - June 19

June 18 - June 19 -

AI Hardware & Edge AI Summit Europe

June 18 - June 19London United Kingdom

June 18 - June 19London United Kingdom -

AI Hardware & Edge AI Summit 2024

September 10 - September 12San Jose CA United States

September 10 - September 12San Jose CA United States -

CDAO Government 2024

September 18 - September 19Washington DC United States

September 18 - September 19Washington DC United States