November 21, 2019

Alternative Data Goes Mainstream in Financial Services

(Tetiana Yurchenko/Shutterstock)

Hundreds of years of financial transactions have created well-worn paths for commerce to be conducted. Companies have been quite comfortable operating within the limits defined by these routes, largely because they’re well-known and everybody agrees on them. But the e-commerce explosion has not only blown up the old transaction paths, but it’s giving companies new data sources from which to make decisions. This is the heart of the alternative data revolution.

Wall Street is designed to reward those who find better ways of assessing risk, and punish those who don’t. Investment firms zealously protect their own data, but are constantly seeking new sources of data that will give their quantitative analysts an edge in decision-making. There’s a lot of structured market data that’s freely available on the Web, and still other data sets that are available with a subscription. But firms that want to truly differentiate themselves are now looking to alternative data for competitive advantage.

Alternative data is any non-standard piece of data that can be used to inform decision-making. That could include data scraped from the Web, from social media, geo-spatial data from telecom providers, weather data, and even photographs taken from drones or satellites. Alternative data is not strictly relegated to the financial services domain, but it’s quite often associated with the quantitative work of banks, hedge funds, and other financial firms.

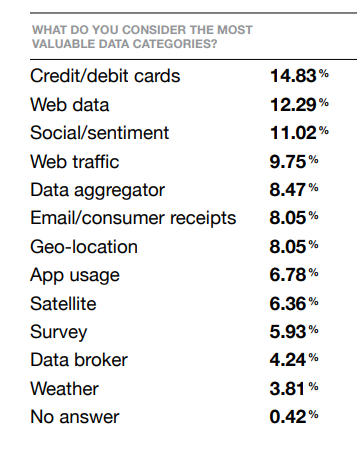

The most valuable categories of alternative data for data buyers, according to a 2019 study by BattleFin and AlternativeData.org

The alternative data space is growing quickly. According to a 2018 study by the trade group AlternativeData.org, investment firms spent $373 million acquiring data sets and hiring employees to analyze them in 2017, which was a 60% increase from the year before. The group’s latest estimates peg the alternative data market driving over $1 billion in spending this year, and growing to $1.7 billion next year.

Other estimates of the alternative data landscape are even higher. The research firm Opimas pegged the total spending on alternative data – including all the software, hardware, and personnel needed to mine it – at $4 billion, growing to $7 billion by 2020. Clearly, this is a market that’s on the move, with more than 400 alternative data providers, according to AlternativeData.org.

These data providers will work to make raw alternative data more consumable, the company says. “Market data vendors are positioned to act as aggregators of fragmented data sources and to provide services that directly tie the alternative data to tradable instruments,” Opimas wrote in a 2017 brief.

FICO Scores Alternative

Hedge funds seeking alpha may be the biggest consumers of alternative data currently. In a sign that alternative data is going mainstream, FICO and Equifax recently announced an expansion of their partnership that involves putting alternative data into the hands of banks, where it can be used to enhance decision-making in a range of use cases.

According to Bill Waid, FICO’s GM Decision Management, alternative data sourced by Equifax is being made available and consumed within FICO’s Decision Management Suite to inform consumer lending and anti-money laundering (AML).

“We sought to bring those two worlds together in a seamless integrated manner so that our clients who are using our decisioning and analytics capabilities, in concert with Equifax data and analytics, could connect and measure continuous improvements by the inclusion of alternative data sources,” Waid told Datanami recently. “That connected value proposition formed the backbone of bringing our two worlds together.”

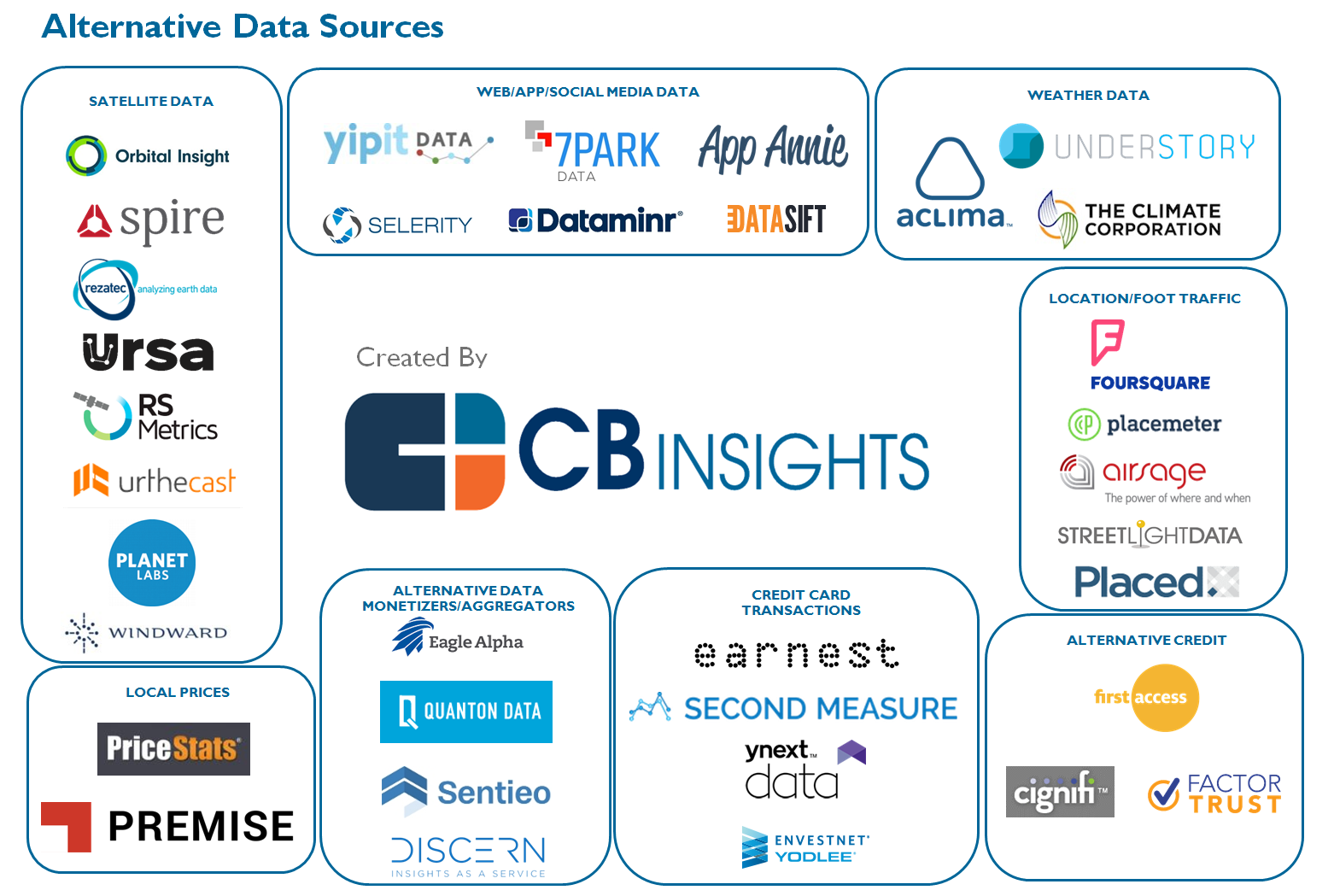

Alternative data sources are flourishing across a range of categories (image courtesy CB Insights)

For banks and other companies that make consumer loans, having alternative data readily available not only impacts decisions around risk, but the entire underwriting process, Waid said.

“Instead of identifying potential credit offers to consumers based solely on a credit score value, we can actually pull the alternative data…and thereby get very specific around the offers that can be made,” Waid said. “And from a financial inclusion perspective, [we can include] alternative data that could potentially extend credit to other people who might have been passed over just because their credit score.

FICO customers will now have ready access to a range of Equifax data packages directly inside their Data Decisions environment, including “industry-specific alternative data scores” for companies that routinely extend credit, including consumer banking, automotive, and communications.

According to Waid, one of the new alternative data sources FICO customers will get access to is an income verification score.

“It’s very useful, particularly in lower credit score situations, [where] you might have a lower credit score, but you have income streams that are not considered in the normal credit offer,” he said. “We can now consider that. There’s also information about tenure at job. There’s a whole suite of them that get included in the actual decisioning process.”

‘Credit Invisibles’

Almost 92 million consumers in the U.S. either have no credit file or have insufficient information in the file to generate a traditional credit score, according to Equifax.

“These ‘credit invisibles’ can range from millennials just entering the workforce to recent immigrants who have not yet established credit,” the company says on its website. “By giving you increased detail around consumer transactions and financial behaviors outside the traditional credit file, alternative data can help you see beyond traditional credit to discover emerging risk and opportunity, expand your current customer relationships, and grow your business.”![]()

FICO is also using alternative data provided by Equifax to improve the AML process at consumer banks. As regulators ramp up scrutiny of transactions, it’s putting a burden on banks to decide whether a transaction is an attempt at money laundering or not. FICO’s software, fueled with Equifax’s data, can help accelerate the identification of potentially fraudulent activity.

“Regulators are asking for more scrutiny, so there’s an inclusion of more transaction types, more account types, that actually get brought into the mix, and that means more manual labor on behalf of a financial institution to go and document and provide evidence back,” he said. “Insofar as we can actually very quickly and automatically [provide] a score that actually shows that it’s not AML, and provide the associated documentation, it’s going to relieve that pressure.”

In many cases, the story of alternative data parallels that of big data itself. It’s relatively new, it’s from a diverse range of sources, and it’s often unstructured. As organizations get more alternative data use cases under their belt, it will not only embolden them to expand their usage, but it will solidify the data workflows and access patterns around it. That’s how ecosystems are established and grow, and that’s currently the case with big, alternative data.

Related Items:

Machine Learning Market Demonstrates Solid Growth

Can AWS Crack the Code for Data Exchanges?

From First to Third, and Alternative Too: A Guide to Data Types

Applications:

Data Mining

Technologies:

Cloud

Leading Solution Providers

Tabor Network

Sponsored Multimedia

Featured Events

-

Call & Contact Center Expo

April 24 - April 25Las Vegas NV United States

April 24 - April 25Las Vegas NV United States -

AI & Big Data Expo North America 2024

June 5 - June 6Santa Clara CA United States

June 5 - June 6Santa Clara CA United States -

AI Hardware & Edge AI Summit 2024

September 10 - September 12San Jose CA United States

September 10 - September 12San Jose CA United States -

CDAO Government 2024

September 18 - September 19Washington DC United States

September 18 - September 19Washington DC United States